What are Payroll Liabilities?

When it comes to paying your staff, as a small business, you want to have as few issues as possible. Understanding the basics of how your payroll accounts work is one of the first steps towards minimising difficulties. Payroll liabilities are an important component of your accounting system since they are derived from the money that employees receive in the form of paychecks. Despite some companies prefer to choose an agency to manage payroll and payroll responsibilities, it is equally critical for business owners to understand how the accounting system works. This entails comprehending the concept of payroll obligation and how it should be managed.

What Are Payroll Liabilities?

Payroll is recorded in two accounts: expense and liability. Your employees are compensated for their labour each pay period based on their salary or hourly payment. The amount owed to your employees per pay period, commonly known as their gross pay, is an expense that needs to be recorded on the payroll expense account. This is not the same as your payroll liabilities.

Payroll liabilities are payroll-related obligations that you need to make for your company. Employee-earned earnings that have yet to be paid, employee taxes, and payroll service charges are examples of liabilities.

Payroll liabilities exist with every payroll you process. However, most businesses meet their payroll obligations on time.

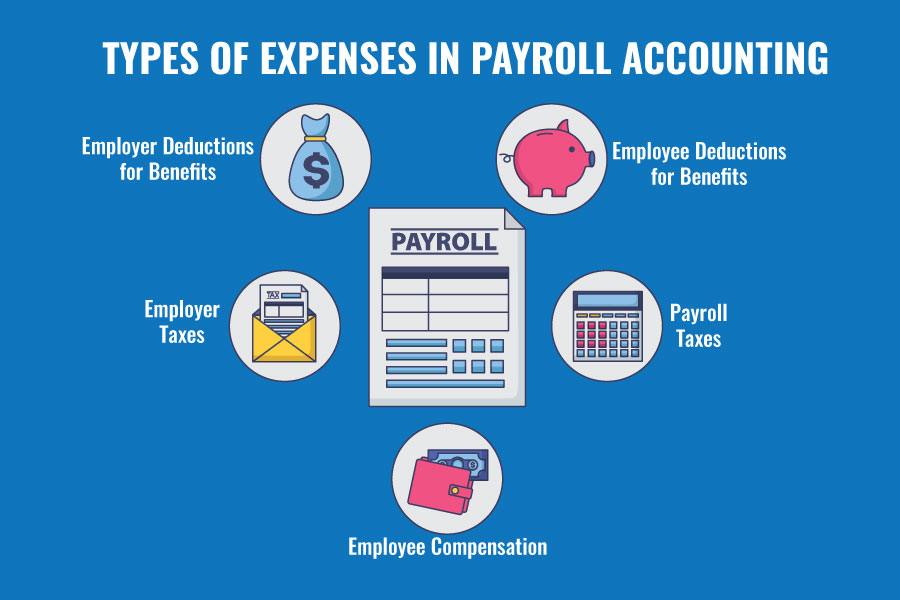

Types of Payroll Liabilities

- Compensation

Regular wages and salaries are part of employee compensation. Overtime pay, retroactive pay, back pay, severance pay, awards, bonuses, commissions, prizes, and accumulated sick leave pay are all types of employee compensation. Include fringe benefits such as health insurance, retirement plans, and paid vacation and personal days when calculating your payroll liabilities.

- Withholding

The mandatory withholding you deduct from your employees’ paychecks stays a liability until the payment is submitted to the appropriate agency. Federal and, if applicable, state and municipal income taxes; Social Security and Medicare taxes; and, if applicable, wage garnishments and state unemployment and disability insurance are all examples of withholding. Employee contributions for voluntary benefits, such as health, life, and disability insurance; retirement plans; adoption assistance; and flexible spending accounts, are classified as liabilities until the funds are paid to the relevant vendor.

- Employer Taxes and Insurance

Social Security and Medicare taxes, as well as federal and state unemployment taxes, are all part of your liabilities. Depending on where you live, the state and municipal governments may levy additional taxes on you, such as a job training tax and a local payroll tax. The state may also require you to carry workers’ compensation insurance. Your share of taxes and insurance remains an obligation until you pay it to the appropriate agency.

- Payroll Service Costs

Wages and taxes aren’t the only payroll-related obligations you have. Unless you do your payroll by hand, you need to pay for payroll software or a PEO (professional employer organisation). These are responsibilities that you incur and are obligated to pay. The company may bill you in arrears if you use software. That is, you utilise the service for a month and then pay at the end of the month or the next month. Until you pay, this is considered a liability.

- Documentation – Keeping & Recording

Document your payroll expenses and liabilities in your company’s payroll or general journal to assist ensure accurate financial records. Make a separate payroll entry as a debit to reflect your overall wage and salary expense for the pay period. Then, as credits, list your employees’ withholdings according to type. The amount of your credits should equal the total of your debits. Make a separate entry to capture your liability share. In this scenario, record the total of your payroll taxes and insurance premiums as a debit. Then, state them individually as credits. The amount of your credits should equal the total of your debits.You also need to maintain track of your deadlines for paying liabilities in order to prevent missing them. Payroll should be processed using a dependable method. You don’t have to worry about wage or tax estimates if you use software. Furthermore, if you choose full-service payroll, you won’t have to worry about depositing your payroll tax liability. Payroll software such as QuickBooks, ADP, Gusto, and Paychex can assist you with wage and tax computations, deposits, and payroll-related document storage.

Keep copies of any payroll-related papers. Make sure they include dates so you know when your liabilities arose and when they are due. You may also set reminders to remind yourself to meet deadlines.

Reconciling Payroll Liabilities

Payroll reconciliation double-checks your mathematical calculations to guarantee that your employees are correctly compensated. To do so, compare your payroll register to the amount you are paying the employee in cash, cheque, direct deposit, or another manner.

Here’s how to perform a payroll reconciliation:

- Examine the payroll register, which contains all of the payroll data

- Collect your employees’ time-tracking data, such as time cards and timesheets

- Check your employees’ pay rates, whether hourly or salary

- Confirm each worker’s deductions

- In the general ledger, record wages and deductions

- Submit payroll

Final Thoughts

Payroll obligations are common in everyday business. It’s easy to become overwhelmed by the complexities of payroll, whether you’re in charge of a team of employees, paying for a payroll service, or facing federal agency fines.