What Are Liabilities in Accounting?

Recent Posts

To run a profitable company, you must have a firm hold on your finances. Although accounting software or an accountant will help you with a lot of the heavy lifting, you should also be aware of the most important aspects of your finances. Liabilities are one of the most crucial aspects to comprehend. Knowing what you owe and who you owe it to is key to running a successful company.

What are liabilities in accounting?

Defined by the International Financial Reporting Standards (IFRS) Framework: “A liability is a present obligation of the enterprise arising from past events, the settlement of which is expected to result in an outflow from the enterprise of resources embodying economic benefits.”

Liabilities, in other words, are claims, whether they are due in six days or six years. Loans, outstanding invoices and other payments, staff salaries, and all other loans that must be paid off ultimately fall into this group.

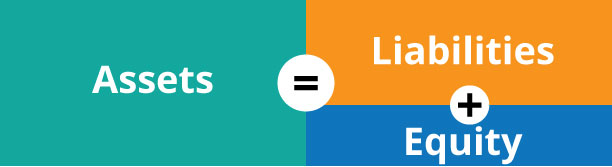

Liabilities differ from assets in accounting because, while assets can be money owed to your company by someone (such as accounts receivable), liabilities are something you owe to someone else. You’re left with shareholder value after subtracting the company’s nett liabilities from its cash.

Source: Market Business News

Types of liabilities

Wages owed to contractors, overdue mortgages, dealer payments, and delinquent taxes are only some of the particular things that may constitute liabilities for small businesses. However, depending on whether they may be repaid, all liabilities are known as current (or short-term) liabilities, long-term liabilities, and contingent liabilities.

- Current/short-term liabilities: These are loans that must be paid within a year by the company. Management should maintain a close eye on current liabilities and insure that the company has enough capital from current investments to meet the loans or commitments.

Examples of current liabilities:

Accounts payable, interest payable, income taxes payable, short-term loans, payroll payments, staff benefits, and vendor invoices

Current liabilities is a crucial component of many short-term liquidity metrics that assess how a company is performing financially. The following main ratios are used by management teams and analysts to do financial reporting and assess businesses:

- The current ratio : Current assets divided by current liabilities

- The quick ratio: Current assets minus inventory divided by current liabilities

- The cash ratio: Cash and cash equivalents divided by current liabilities

- Non-current liabilities, also known as long-term liabilities, are loans that you do not have obligation to pay off over the next 12 months. Long-term liabilities are a crucial component of a company’s long-term finance strategy. Long-term debt is taken out by companies to obtain urgent funding to finance the acquisition of capital assets or to invest in new capital ventures.

Long-term obligations play a critical role in assessing a company’s long-term viability. Companies will face a solvency crisis if they are unable to repay their long-term loans when they become due.

Examples of non-current liabilities:

Term loans, lines of credit, pension obligations, and other deferred employment payments

- Contingent liabilities are obligations that may arise as a result of a future event. As a result, contingent liabilities are liabilities that may arise in the future. For example, if a company is facing a $155,000 lawsuit, the company will be liable if the lawsuit is successful. However, if the lawsuit is unsuccessful, there will be no liability. A contingent liability is only recorded in accounting standards if the liability is likely (defined as more than 50 percent likely to happen). It is possible to estimate the amount of the resulting liability.

Examples of contingent liabilities

Lawsuits, product warranties

A organisation may accumulate liabilities in a variety of ways, each with various long- and short-term financial consequences. So, in addition to understanding what liabilities are and which ones you have, it’s important to consider how each of them functions so you can see how they change the cash flow from month to month.

How to calculate liabilities

You can measure the company’s obligations in a few different ways, but the most popular method is to simply sum up all of the current short- and long-term debts.

To do so, you’ll need to first figure out how much you owe on each of your company’s individual liabilities. You will do this by subtracting the overall sum spent to date from the original balance.

Initial Balance – Total Paid to Date = Remaining Liability

Another method for calculating liability is to take the total value of the company’s assets and subtract shareholder equity (the net value of the business). This leaves you with the overall amount owed by the company (liabilities).

Usually, this calculation is normally reversed, with shareholder value measured by subtracting liabilities from net assets, although it is theoretically possible to quantify liabilities in this manner using accounting rules.

Total Assets – Shareholder Equity = Total Liabilities

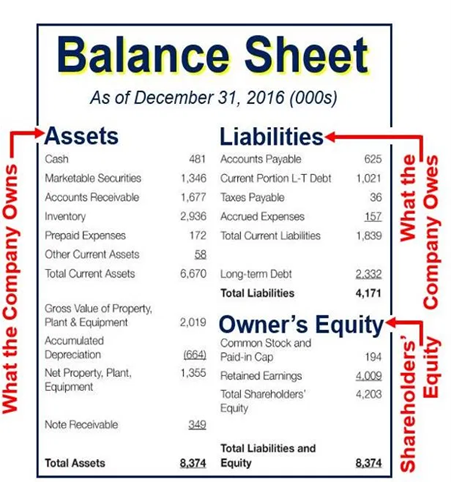

Here is a quick example of the balance sheet where you can find the main types of the liabilities that the small business might face.

Source: Planium Pro software

Liabilities vs expenses

From an accounting standpoint, it’s important to consider the distinctions between liability and expense. Unfortunately, since liabilities and expenses are also correlated with spending, it can be complicated.

A liability is money owed to buy an item, such as a loan for new office equipment. According to The Balance, expenses are recurring payments on anything that has no physical worth except for a facility. Expenses are often reported in the income statement rather than the balance sheet. Both claims are financial in nature.

A monthly company mobile phone bill is an example of an expense. However, once you’re stuck into a deal and must pay a cancellation charge to get out, the fee would be classified as a liability. Your store’s utilities are an expense. Your store’s mortgage is a liability.

Now that you know what liabilities are and what kinds of liabilities exist, you can help assess how your small company is doing financially in the short and long term.

Other Resources

- ‘What is a Liability?’ – https://corporatefinanceinstitute.com/resources/knowledge/finance/liability/

- ‘Definition and Recognition of the Elements of Financial Statements’ (PDF). Australian Accounting Standards Board. (https://www.aasb.gov.au/admin/file/content102/c3/SAC4_3-95.pdf)

- ‘US Small Business Administration sample spreadsheet for a small business’. Archived from the original on 2007-07-15. (https://web.archive.org/web/20070715223932/http://www.sba.gov/library/balsheet.xls)

- ‘Presentation of Financial Statements’ International Accounting Standards Board. http://www.iasplus.com/standard/ias01.htm

- ‘IFRS VS GAAP: BALANCE SHEET AND INCOME STATEMENT’ (web). Accounting-financial-tax.com. (http://accounting-financial-tax.com/2008/06/ifrs-vs-gaap-balance-sheet-and-income-statement/)